07. Executors

Because a DEX operates on top of a blockchain, it follows the basic principle of blockchains: there is a decentralized ledger of transactions which validators are building. So, one can see a DEX as an evolving state of a sequential computer.

As was explained in chapter 6, we fixed a certain set of transaction types and we fixed their semantics for all but one.

The single exceptional case being add-order transaction.

On the technical level, a single add-order execution must be resolved to a sequence of swaps. This is the job of

an executor. We consider an executor to be pluggable part of DEX implementation.

In this chapter we specify the algorithms of all executors currently supported in Dexter. The dynamic behaviour of these algorithms and especially the comparative measurements of their statistics is the primary motivation behind creating Dexter.

Space of executors research

The space of all possible executor is vast. Dexter was created as a proof of concept tool for investigating the contents of this space.

However, in the current version of Dexter, we limit our attention to rather “simplistic” class of executors, specifically, we require executors to be compliant with the following rules:

- Rule #1: Equality of traders

Swaps chronology can depend only on the state of markets (i.e. it is not allowed that it depends on the state of traders).

This rule means that the exchange in not “biased” on trader’s identity or other trader properties (such as wealth of a trader for example). In lame terms it means that all traders are considered “equally important” by the executor - i.e. from the perspective of an executor, any trader is seen as “just an account number” (similar concept to “all citizens are considered equal by law in a democracy”). In particular - current balance of trader’s account, past history of his trading activity and trader’s name - all this cannot influence the path of DEX evolution that an executor is creating.

- Rule #2: Isolation of markets

Arrival of a new order generates swaps only on the market where this order belongs to.

- Rule #3: Isolation of traders

Every swap involves only one order.

- Rule #4: Isolation of swaps

An executor makes next-swap decision based only on the current state of the market and number of swaps executed in the current executor loop. The intention here is that the executor is not allowed to decide based on the history of executes swaps.

- Rule #5: Natural trading priority

Execution prioritizes traders happy to accept less attractive exchange rate (i.e. an exchange rate that gives him less profit). In case of a tie, a trader waiting longer is served first.

- Rule #6: Funds locking

Trader can place an order on the DEX only if the amount of tokens to be sold is covered by the balance of his account. Upon placing an order, the executor will issue a “lock” on the amount of tokens declared in the order as sell amount. Locked tokens cannot be reused in another order. Locked tokens get unlock on order expiration or cancellation.

Motivation for above rules comes from various sources:

Equality of traders and Natural trading priority seem to be very natual and go along the general expectations of the wide public; any DEX violating these rules would be really a weird one.

Funds locking is a business-level decision; DEXes violating this rule are probably quite useful and interesting, although it must be said that their trading mechanics would be more distant from Forex tradition. Therefore the motivation behind funds locking can be seen as “let’s keep things mentally close to Forex community for now” (please notice that Dexter is all about simulating hybrid exchanges, so the analogy to Forex is going to be always around).

All 3 “isolation” rules delineate the boundary of “simplest executors one can consider”; anything beyond this region immediately becomes complex and sophisticated. From this perspective the mission of Dexter can be understood as “let’s see how far we can get with those simplistic executors before we delve into sophisticated ones”. A good motivation for dropping isolation of markets would be building a DEX where arbitrage is impossible. A good motivation for dropping isolation of traders would be borrowing from Forex the idea of direct trader-to-trader swaps, i.e. bypassing the AMM interaction when possible.

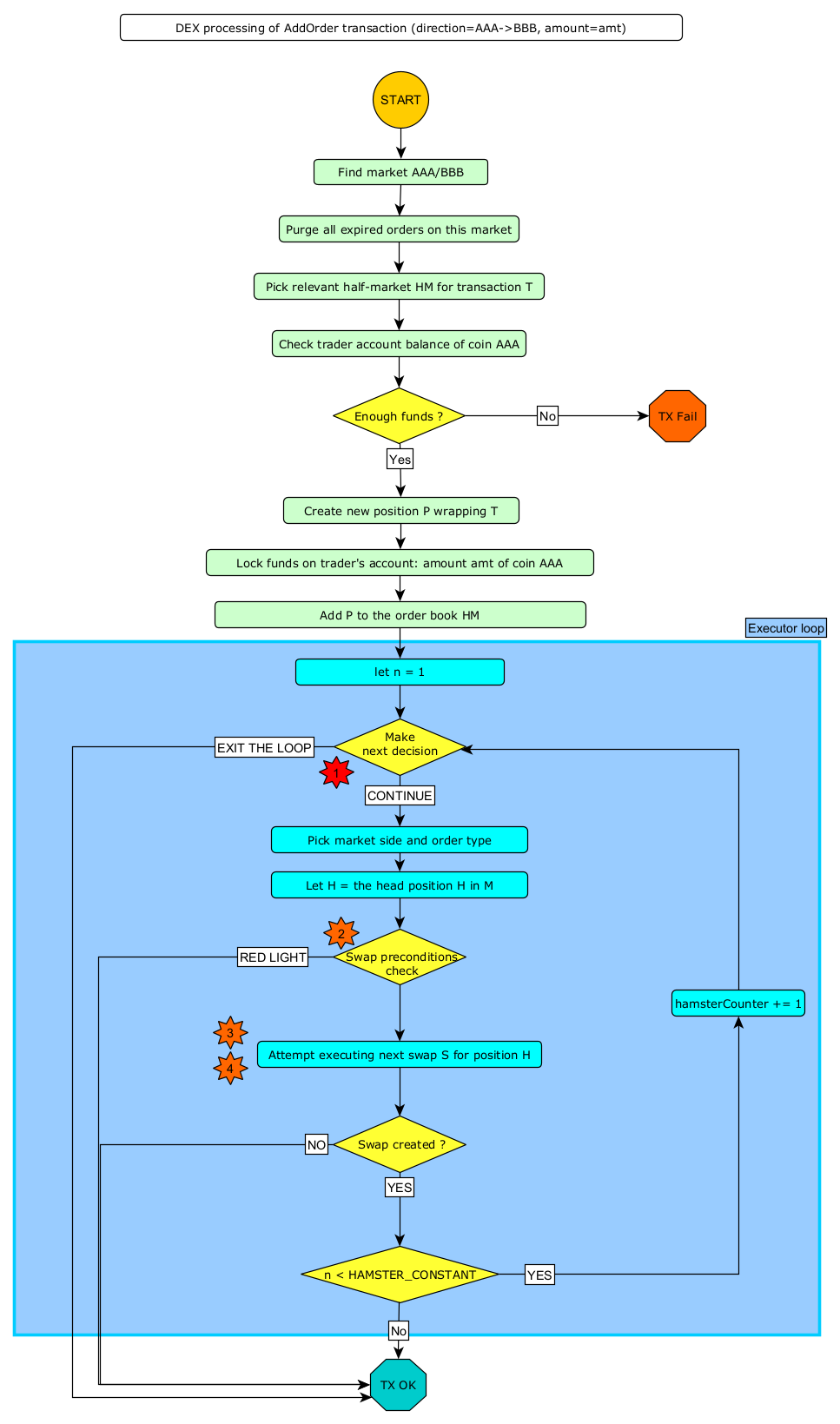

Executor loop overview

Because we assume Rule #2: Isolation of markets, once a new order arrives to the DEX, we are going to process

the order book only for the market where the new order belongs. Let us fix the coins to be \(AAA\) and \(BBB\),

so the market is \(AAA/BBB\) and orders have direction \(AAA \rightarrow BBB\) or

\(BBB \rightarrow AAA\). We will further refer to this market as market (see the scripts below).

Thanks to the rules enumerated in previous chapter, the job of an executor loop can be largely simplified. Let us outline the template of such loop by extending the activity diagram in from previous chapter:

Places marked above with red asterisk are where non-trivial logic must be plugged-in:

- 1: Making next executor decision

At this point, one of two half-markets must be picked. This is equivalent to selecting a direction: \(AAA \rightarrow BBB\) or \(BBB \rightarrow AAA\). In the context of “oriented” market, this means selecting “asks” or “bids” side of the order book. Additionally, the order type (

LimitvsStop) must be selected here. An executor is free to give up at this point, if the state of the market does not allow for executing of any order.- 2: Checking swap preconditions

At this point swap preconditions are checked. Red light will abort swap creation and terminate the executor loop.

- 3: Calculating swap amount and executing the swap

Deciding on amounts of the next swap to be executed. Because of Rule #5: Natural trading priority, the next swap to be executed must be for the head position on the positions collection (because the positions list is ordered by price-then-order-time).

- 4: Post-swap assertions

Extension point for plugging-in diagnostic assertions to be checked after every swap.

Arithmetic precision problems and their solution

Internal working of the executor is vulnerable to “strange” effects caused by imperfectness of computer arithmetic. This effects generally disrupt the operation of mathematical definitions of the executor. Two particular problems are:

- When (at least one side of) the AMM balance becomes small enough, integer rounding effects can cause significant

errors in calculated swap amounts.

When calculated swap amounts are small enough, integer rounding may cause limit-price invariant to fail.

To avoid such anomalies we generally apply a simple approach:

Enforce that AMM balances are always above certain AMM_MIN_BALANCE (which is a parameter).

Enforce that order amount is always above certain TRADING_MIN_AMOUNT (which is a parameter).

Enforce that swap amounts are always above certain SWAP_MIN_AMOUNT (which is a parameter).

To work as expected, above parameters must be set accordingly to the arithmetic precision used by the implementation of DEX. Please notice that arithmetic precision is also limited in the fixed-point arithmetic - because of the necessary rounding in operations such as multiplication.

For example if the arithmetic precision is at the order 1e-18, then “reasonable” values for above params could be:

AMM_MIN_BALANCE = 1e-14

TRADING_MIN_AMOUNT = 1e-8

SWAP_MIN_AMOUNT = 1e-10

Executor loop details

The general pattern of open-order processing is implemented in class ExecutorTemplate. The executor loop is part

of this:

def open(order: Order): Unit = {

//log diagnostic info "new order arrived"

if (coreCallsDump.isDefined)

coreCallsDump.get.print(s"[btime $blockchainTime] [rtime ${clock.apply()}] open order: id=${order.id} type=${order.orderType} account=${order.accountAddress}" +

s" askCoin=${order.askCoin} bidCoin=${order.bidCoin} price=${order.exchangeRate.toDouble} amount=${order.amount} exptime=${order.expirationTimepoint}")

//check if the account address if valid

precondition(hash2account.contains(order.accountAddress), s"unknown account: ${order.accountAddress}")

//decode account address to account instance

val account: Account = hash2account(order.accountAddress)

//find relevant market and half-market

val coinPairAB: CoinPair = CoinPair(order.askCoin, order.bidCoin)

val halfMarketAB: HalfMarket = coinPair2HalfMarket(coinPairAB)

val market: Market = coinPair2Market(coinPairAB.normalized)

//purge expired orders on this market

purgeExpiredPositionsOnMarket(market)

//check if the trader has enough funds to place this order

precondition (order.amount <= account.getFreeBalanceFor(order.sellCoin), s"order amount exceeds free balance for this account and coin: ${account.getFreeBalanceFor(order.sellCoin)}")

//create new position instance (wrapping the order)

val position = Position(order, market, account, blockchainTime, clock.apply())

hash2position += order.id -> position

//lock amount of tokens on trader's account corresponding to sell amount of this order

account.addPosition(position)

//add position to the order book

halfMarketAB.addPosition(position)

//update statistics

market.onPositionOpened(position)

//log diagnostic info "new position added"

if (coreCallsDump.isDefined)

coreCallsDump.get.print(s"[btime $blockchainTime] [rtime ${clock.apply()}] created new position for order ${position.id} normalized-amount=${position.normalizedAmount} normalized-price=${position.normalizedLimitPrice.toDouble}")

//executor loop

var n = 1

var lastDecision: Option[(MarketSide, OrderType)] = executorNextDecision(market, position)

var lastExecutionWasOk: Boolean = true

while (n <= hamsterConstant & lastDecision.nonEmpty && lastExecutionWasOk && market.isAmmBalanceAboveTradingMinimum) {

lastExecutionWasOk = lastDecision match {

case Some((MarketSide.Asks, OrderType.Limit)) => attemptCreatingNextSwap(n, market, market.halfMarketAsks, OrderType.Limit)

case Some((MarketSide.Bids, OrderType.Limit)) => attemptCreatingNextSwap(n, market, market.halfMarketBids, OrderType.Limit)

case Some((MarketSide.Asks, OrderType.Stop)) => attemptCreatingNextSwap(n, market, market.halfMarketAsks, OrderType.Stop)

case Some((MarketSide.Bids, OrderType.Stop)) => attemptCreatingNextSwap(n, market, market.halfMarketBids, OrderType.Stop)

}

n += 1

if (lastExecutionWasOk)

lastDecision = executorNextDecision(market, position)

}

}

Extension points - marked previously as red asterisks on the diagram - are encoded as corresponding abstract methods. For implementing a specific executor, one needs to provide implementation of these methods only:

def executorNextDecision(market: Market, newPositionThatTriggeredTheLoop: Position): Option[(MarketSide, OrderType)]

def swapPreconditionsCheck(

market: Market,

halfMarketAB: HalfMarket,

askCoin: Coin, //buy coin

bidCoin: Coin, //sell coin

position: Position, //position for which the swap is to be executed

a: FPNumber, //AMM balance of ask coin

b: FPNumber, //AMM balance of bid coin

r: Fraction, //limit price as declared in the order

ammPrice: Fraction): Decision

//returns (sellAmount, buyAmount) - where sell/buy meaning is from the perspective of the trader

def calculateSwapAmounts(

market: Market,

halfMarketAB: HalfMarket,

askCoin: Coin, //buy coin

bidCoin: Coin, //sell coin

position: Position, //position for which the swap is to be executed

a: FPNumber, //AMM balance of ask coin

b: FPNumber, //AMM balance of bid coin

r: Fraction, //limit price as declared in the order

ammPrice: Fraction): (FPNumber, FPNumber)

def postSwapAssertions(

market: Market,

halfMarket: HalfMarket,

position: Position,

sellAmount: FPNumber,

sellCoin: Coin,

buyAmount: FPNumber,

buyCoin: Coin,

ammPriceBeforeSwap: Fraction): Unit

Most complex part is the “attempt to create next swap”. This was not covered in detail on the diagram above:

def attemptCreatingNextSwap(hamsterLoopIteration: Int, market: Market, halfMarketAB: HalfMarket, orderType: OrderType): Boolean = {

val askCoin: Coin = halfMarketAB.coinPair.left

val bidCoin: Coin = halfMarketAB.coinPair.right

lazy val headPosition: Position = orderType match {

case OrderType.Limit => halfMarketAB.limits.head

case OrderType.Stop => halfMarketAB.stops.head

}

val a: FPNumber = market.ammBalanceOf(askCoin)

val b: FPNumber = market.ammBalanceOf(bidCoin)

val r: Fraction = headPosition.exchangeRate

val ammPrice: Fraction = market.currentPriceDirected(askCoin, bidCoin)

if (coreCallsDump.isDefined)

coreCallsDump.get.print(s"limit-execute: (iteration $hamsterLoopIteration) askCoin=$askCoin [balance $a] bidCoin=$bidCoin [balance $b] directed-amm-price=${ammPrice.toDouble}" +

s" head-position=${headPosition.id} outstanding-amount=${headPosition.outstandingAmount} limit-price=${FPNumber.fromFraction(r)}")

swapPreconditionsCheck(market, halfMarketAB, askCoin, bidCoin, headPosition, a, b, r, ammPrice) match {

case Decision.GREEN =>

val (sellAmount, buyAmount): (FPNumber, FPNumber) = calculateSwapAmounts(market, halfMarketAB, askCoin, bidCoin, headPosition, a, b, r, ammPrice)

//negative amounts are considered a bug in 'calculateSwapAmounts'

assert(sellAmount >= FPNumber.zero && buyAmount >= FPNumber.zero, s"calculateSwapAmounts() returned negative value: sellAmount=$sellAmount buyAmount=$buyAmount")

//avoid "nano" swaps (below SWAP_MIN_AMOUNT), unless this is a complete filling case

if (sellAmount <= swapMinAmount || buyAmount <= swapMinAmount)

if (headPosition.amount > swapMinAmount)

return false

//zero amount is not considered a bug in 'calculateSwapAmounts', but we will not proceed with swap execution

if (sellAmount == FPNumber.zero || buyAmount == FPNumber.zero)

return false

//we need to distinguish between partial filling and complete filling

if (headPosition.amount == sellAmount) {

//case 1: complete filling

if (coreCallsDump.isDefined)

coreCallsDump.get.print(s"executor decision: complete filling of $headPosition")

val normalizedAmount: FPNumber = headPosition.normalizedAmount

headPosition.registerCompleteFilling(sold = sellAmount, bought = buyAmount, blockchainTime)

orderType match {

case OrderType.Limit => halfMarketAB.limits.removeElementAtIndex(0)

case OrderType.Stop => halfMarketAB.stops.removeElementAtIndex(0)

}

market.onPositionFilled(headPosition, normalizedAmount)

headPosition.account.removePosition(headPosition)

dumpFillingInfo(headPosition, sold = sellAmount, bought = buyAmount, isCompleteFilling = true)

} else {

//case 2: partial filling

if (coreCallsDump.isDefined)

coreCallsDump.get.print(s"executor decision: partial filling of $headPosition")

val oldNormalizedAmount: FPNumber = headPosition.normalizedAmount

headPosition.registerIncompleteFilling(sold = sellAmount, bought = buyAmount, blockchainTime)

val delta: FPNumber = oldNormalizedAmount - headPosition.normalizedAmount

market.onPositionPartiallyFilled(headPosition, delta)

dumpFillingInfo(headPosition, sold = sellAmount, bought = buyAmount, isCompleteFilling = false)

}

//update statistics

swapExecutionsCounter += 1

//update account balances (to reflect the swap execution)

headPosition.account.updateBalance(bidCoin, sellAmount.negated)

headPosition.account.updateBalance(askCoin, buyAmount)

//update the liquidity pool (to reflect the swap execution)

market.updateLiquidityPool(bidCoin, sellAmount)

market.updateLiquidityPool(askCoin, buyAmount.negated)

//accumulation of some statistics for the AMM

tokensExchangedIn.increment(bidCoin, sellAmount)

tokensExchangedOut.increment(askCoin, buyAmount)

//extension point for more assertions

postSwapAssertions(market, halfMarketAB, headPosition, sellAmount, bidCoin, buyAmount, askCoin, ammPrice)

//we completed the swap with success

return true

case Decision.RED =>

//abort the swap

return false

}

}

Variant 1: TEAL executor

This executor is based on a proprietary algorithm created in Onomy Protocol. This executor follows this TLA+ specification:

https://github.com/onomyprotocol/specs/

On top of the specification we apply the “minimal trading balance” check on the AMM level. We just do not allow either size of the liquidity pool to

1. Executor next decision

We select the same half-market where the position belongs.

In this variant, the value of HAMSTER_CONSTANT is hardcoded to 1, so the executor loop has always at most 1 iteration.

override def executorNextDecision(market: Market, newPositionThatTriggeredTheLoop: Position): Option[(MarketSide, OrderType)] =

Some(newPositionThatTriggeredTheLoop.normalizedMarketSide, newPositionThatTriggeredTheLoop.orderType)

2: Swap preconditions check

The head of order book is ready for next swap if the current value of ammPrice exceeds the limit price of the order.

Please notice that we compare prices calculated in the same direction.

override def swapPreconditionsCheck(

market: Market,

halfMarketAB: HalfMarket,

askCoin: Coin,

bidCoin: Coin,

position: Position,

a: FPNumber,

b: FPNumber,

r: Fraction,

ammPrice: Fraction): Decision = {

position.orderType match {

case OrderType.Limit => if (ammPrice > r) Decision.GREEN else Decision.RED

case OrderType.Stop => if (ammPrice < r) Decision.GREEN else Decision.RED

}

}

3: Calculate swap amounts

The “magic” formula of swap creation is defined here.

override def calculateSwapAmounts(

market: Market,

halfMarketAB: HalfMarket,

askCoin: Coin,

bidCoin: Coin,

position: Position,

a: FPNumber,

b: FPNumber,

r: Fraction,

ammPrice: Fraction): (FPNumber, FPNumber) =

position.orderType match {

case OrderType.Limit =>

val maxBidAmt: FPNumber = (a - b ** r) ** ((r + 1).reciprocal)

val strikeBidAmt: FPNumber = FPNumber.min(position.outstandingAmount, maxBidAmt)

val strikeAskAmt: FPNumber = strikeBidAmt ** r

(strikeBidAmt, strikeAskAmt)

case OrderType.Stop =>

val minMemberABal: FPNumber = a / FPNumber.fromLong(2)

val maxMemberBBal: FPNumber = a + b - minMemberABal

val maxMemberBAmt: FPNumber = maxMemberBBal - b

val strikeBidAmt: FPNumber = FPNumber.min(position.outstandingAmount, maxMemberBAmt)

val strikeAskAmt: FPNumber = (strikeBidAmt * (a - strikeBidAmt)) / (b + strikeBidAmt)

(strikeBidAmt, strikeAskAmt)

}

Variant 2: TURQUOISE executor

This executor is based on the idea that we execute orders always using the limit price as declared in the order itself - as long as the AMM-price allows to do so without introducing loss on DEX side. This approach is rather “unusual” when compared to FOREX-style exchanges, where the swap price is always the current market price.

Here we allow the HAMSTER_CONSTANT to be arbitrary number bigger than zero.

Caution: STOP ORDERS are not supported.

Math derivation

We consider an execution of some limit order \(BBB \rightarrow AAA\), i.e. where BBB is the bid coin and AAA is the ask coin. In effect of the execution, \(x:AAA\) will be received from AMM and \(y:BBB\) will be given to AMM. After the execution, the new state of the AMM will be:

An order contains a declared limit price \(r\). The execution of an order is only allowed when \(ammprice \geq r\).

Additionally, we want to keep the constant conversion rate for every order and we want it to be equal to the declared limit price. In other words we want the following condition to hold:

Let’s assume that we have an order for which the condition \(ammprice \geq r\) is true. We want to find the maximal amount of swap which is possible.

For the maximal swap, the inequality will turn into equality, hence we will have:

The ammprice after successful execution of the order will be:

Effectively, we arrive to the following system of equations (where \(x\) and \(y\) are unknown):

Solving this leads to:

1. Executor next decision

We check head positions of bids and asks half-markets to understand if they are possibly ready to execute next swap, given the current AMM price value. Only-ask, only-bid and none-of-them are easy cases - we select the only side which is possible. The only tricky case is when both head bid and head ask could be picked for execution in the next step. In such case we pick the one with bigger overhang.

In case of a tie, we use a boolean variable flipper, to pick one side, and then we negate flipper so that

in the case of next tie, the decision will be in favour of the other side.

private var flipper: Boolean = false

override def executorNextDecision(market: Market, newPositionThatTriggeredTheLoop: Position): Option[(MarketSide, OrderType)] = {

if (market.limitOrderBookAsks.isEmpty && market.limitOrderBookBids.isEmpty)

return None

if (market.limitOrderBookBids.isEmpty)

return Some((MarketSide.Asks, OrderType.Limit))

if (market.limitOrderBookAsks.isEmpty)

return Some((MarketSide.Bids, OrderType.Limit))

val topBid: Fraction = market.limitOrderBookBids.head.normalizedLimitPrice

val bottomAsk: Fraction = market.limitOrderBookAsks.head.normalizedLimitPrice

val ammPrice: Fraction = market.currentPriceNormalized

if (topBid <= ammPrice && ammPrice <= bottomAsk)

return None

if (bottomAsk < ammPrice && topBid <= ammPrice)

return Some((MarketSide.Asks, OrderType.Limit))

if (topBid > ammPrice && bottomAsk >= ammPrice)

return Some((MarketSide.Bids, OrderType.Limit))

val bidOverhang = topBid - ammPrice

val askOverHang = ammPrice - bottomAsk

if (bidOverhang > askOverHang)

return Some((MarketSide.Bids, OrderType.Limit))

if (bidOverhang < askOverHang)

return Some((MarketSide.Asks, OrderType.Limit))

//they are equal, so we pick one pointed by the flipper

flipper = ! flipper

flipper match {

case true => return Some((MarketSide.Bids, OrderType.Limit))

case false => return Some((MarketSide.Asks, OrderType.Limit))

}

}

2: Swap preconditions check

Same as in TEAL variant, but without stop orders support.

override def swapPreconditionsCheck(

market: Market,

halfMarketAB: HalfMarket,

askCoin: Coin,

bidCoin: Coin,

position: Position,

a: FPNumber,

b: FPNumber,

r: Fraction,

ammPrice: Fraction): Decision =

if (ammPrice > r)

Decision.GREEN

else

Decision.RED

3: Calculate swap amounts

Following the math derivation above.

override def calculateSwapAmounts(

market: Market,

halfMarketAB: HalfMarket,

askCoin: Coin,

bidCoin: Coin,

position: Position,

a: FPNumber,

b: FPNumber,

r: Fraction,

ammPrice: Fraction): (FPNumber, FPNumber) = {

val x: BigInt = r.numerator

val y: BigInt = r.denominator

val maxBidAmt: FPNumber = FPNumber((a.pips * y - b.pips * x) / (2 * x))

val maxAmountOfBidCoinThatWillNotDrainAmmBelowMargin: FPNumber = (market.ammBalanceOf(askCoin) - ammMinBalance) ** r.reciprocal

val strikeBidAmt: FPNumber = FPNumber.min(FPNumber.min(position.outstandingAmount, maxBidAmt), maxAmountOfBidCoinThatWillNotDrainAmmBelowMargin)

val strikeAskAmt: FPNumber = strikeBidAmt ** r

return (strikeBidAmt, strikeAskAmt)

}